The Grid’s Second Challenge: How Electric Vehicles Are Reshaping Distribution Infrastructure

How managed charging transforms infrastructure burden into rate-reducing asset—and why Norway spent zero on grid upgrades at 94% EV penetration

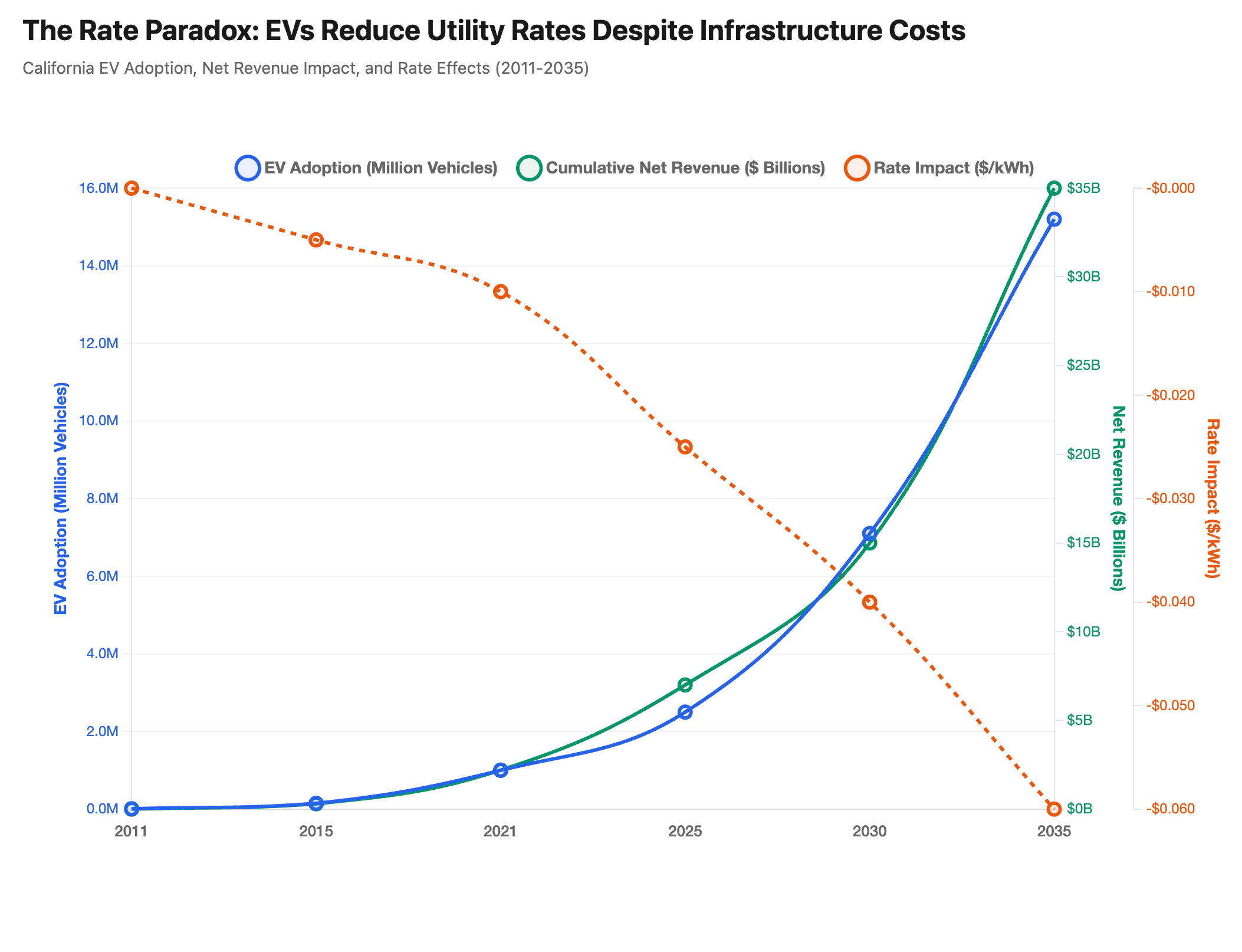

While U.S. policymakers debate EV adoption targets, China has already put more than 20 million electric vehicles on the road—and is racing to prevent peak loads from multiplying sevenfold by 2050.¹ The United States faces a different but equally consequential challenge: California alone has deployed 2.1 million EVs, yet the state projects that 50% of its distribution feeders will overload by 2035 without $6-20 billion in infrastructure upgrades.²

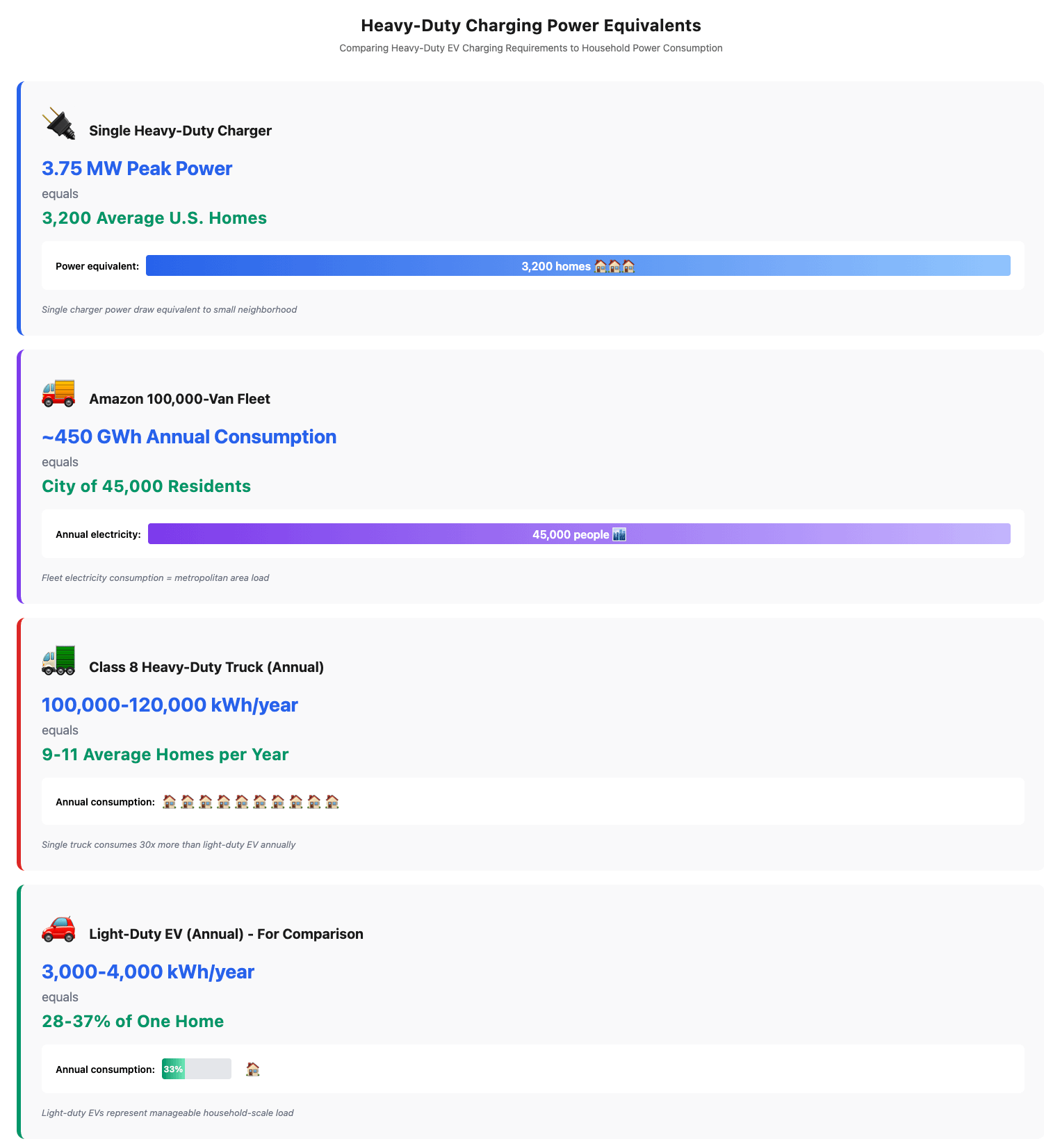

This represents a fundamental grid planning paradox. Despite requiring tens of billions in distribution infrastructure investment, electric vehicle charging creates net downward pressure on utility rates through improved asset utilization. California’s three largest utilities collected $2.2 billion more in revenue from EV customers than it cost to serve them between 2011 and 2021—even while planning massive grid expansion.³ Amazon’s planned 100,000-van fleet will consume as much electricity annually as a city of 45,000 residents, yet that load is flexible, controllable, and potentially bidirectional.

Electric vehicles represent the second major catalyst for U.S. electricity demand growth after data centers, projected to reach 2.5-4.6% of total power demand by 2030.⁴ But the nature of EV load growth differs fundamentally from data centers’ continuous, inflexible baseload. EV charging is inherently schedulable and capable of providing grid services worth up to $1,725 per vehicle annually when properly orchestrated.⁵ Norway’s experience demonstrates that even at 94% EV market penetration, managed charging can reduce infrastructure investment to zero—saving £200 million per 50,000-person city.⁶

The strategic opportunity lies not in preventing EV adoption but in architecting grid integration that transforms distributed vehicle batteries from infrastructure burden into rate-reducing asset.

The Rate Paradox: Infrastructure Costs Meet Utilization Benefits

The most counterintuitive finding in EV grid integration economics is that despite requiring tens of billions in infrastructure investment, electric vehicle charging creates net downward pressure on utility rates. The mechanism is improved grid utilization—spreading fixed infrastructure costs across more kilowatt-hour sales without proportionally increasing peak capacity requirements.

California provides the definitive evidence. Analysis by NRDC and Synapse Energy Economics found that EVs contributed $2.2 billion more in utility revenue than costs to serve between 2011 and 2021.³ Even accounting for substantial infrastructure costs, California experiences a net rate reduction of $0.01-$0.06 per kilowatt-hour from EV adoption—meaning all customers benefit from lower rates, not just EV drivers.³

Customer charging behavior drives this outcome. EV customers on time-of-use rates conduct only 9-14% of charging during on-peak hours, with the vast majority occurring overnight when spare grid capacity exists.³ This load pattern is the key to improved economics: utilizing existing infrastructure during periods when it would otherwise sit idle.

The conditions for rate benefits are specific but achievable: strategic EV charging placement in areas with surplus grid capacity, load management through off-peak charging incentives to avoid peak demand increases, and minimizing unnecessary infrastructure construction through targeted upgrades and managed charging. Load growth must translate to asset utilization improvement rather than merely replicating peak demand patterns.

This creates a strategic planning imperative. Utilities that encourage EV charging in areas requiring infrastructure anyway, or that already have surplus capacity, capture maximum rate benefit. Those that allow uncoordinated charging in constrained areas face infrastructure costs without offsetting utilization gains—transforming a rate-reducing opportunity into a rate-increasing burden.

Yet the paradox persists: even as EVs reduce rates through utilization, they create concentrated distribution infrastructure challenges that require immediate planning action.

The Transformer Crisis: From 30 Years to Three

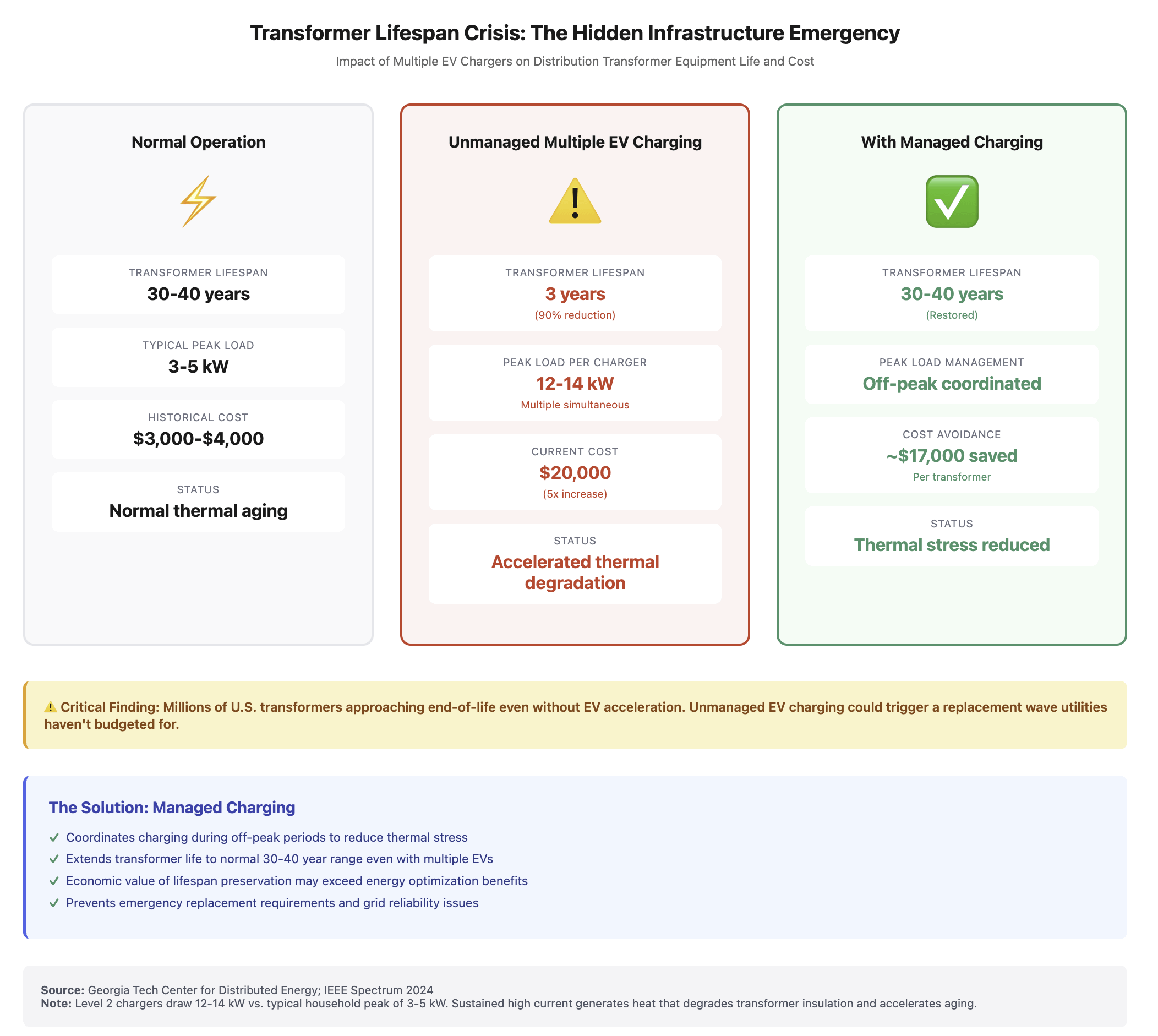

Beyond bulk capacity upgrades, the distribution grid faces an equipment lifespan emergency that threatens to negate managed charging benefits. Research from Georgia Tech’s Center for Distributed Energy demonstrates that multiple Level 2 chargers operating on a single distribution transformer reduce its operational life from the typical 30-40 years to just three years.⁷

The mechanism is thermal stress. A Level 2 charger draws 12-14 kilowatts compared to typical household peak loads of 3-5 kilowatts.⁷ When multiple EVs charge simultaneously on one transformer during evening hours, the sustained high current generates heat that degrades insulation and accelerates aging. The failure mode isn’t gradual—transformers can blow out entirely, requiring emergency replacement.

Transformer economics have deteriorated sharply. Units that historically cost $3,000-$4,000 now run $20,000 each due to supply chain constraints and commodity price inflation—a fivefold increase.⁷ Millions of U.S. transformers are approaching end of designed life even without EV acceleration. Unmanaged EV charging could trigger a replacement wave that utilities haven’t budgeted for and manufacturers can’t fulfill on compressed timelines.

Managed charging directly addresses this vulnerability. Coordinating charging during off-peak periods reduces thermal stress and can extend transformer life to the normal 30-40 year range even with multiple EVs per transformer.⁷ The economic value of this lifespan preservation may exceed the value of energy cost optimization in many utility service territories—a point often overlooked in managed charging business cases.

California’s distribution grid offers the clearest picture of infrastructure requirements at scale. A 2024 study published in the Proceedings of the National Academy of Sciences analyzed more than 5,000 feeders statewide, finding that 50% will experience overload conditions by 2035 and 67% by 2045 under projected EV adoption scenarios.² Distribution system capacity upgrades totaling 25 gigawatts will be required by 2045, at costs ranging from $6-20 billion.²

The state approved $1.4 billion in December 2024 specifically for EV charging infrastructure, bringing total investment in zero-emission vehicle infrastructure to $2.3 billion to date. Current infrastructure stands at 91,000 public and shared chargers against a 2025 target of 250,000 total chargers—indicating the deployment acceleration required.

Heavy-Duty Reality: The 3,200-Home Equivalent

Heavy-duty vehicle charging requirements dwarf light-duty infrastructure and represent the approaching inflection point that will test grid integration strategies. A single heavy-duty vehicle charger draws 3.75 megawatts of peak power—equivalent to 3,200 average U.S. homes.⁸ Fleet charging stations serving ten semi trucks require several megawatts, with larger depots demanding 20 megawatts or more.⁸

Amazon’s Maple Valley warehouse dedicates 3 megawatts of power for chargers. The company’s full 100,000-van fleet suggests approximately 300+ megawatts of total peak charging demand nationwide if unmanaged. FedEx targets 50% of global pickup and delivery vehicles electric by 2025, 100% by 2030. UPS ordered 10,000 electric delivery vehicles. Combined, these three companies’ electrification represents load equivalent to a metropolitan area of 70,000-80,000 residents, concentrated in depot locations requiring distribution infrastructure that doesn’t exist.

Proper overnight charging strategies can reduce power requirements by up to 80% compared to peak charging scenarios.⁸ A fleet of 30 trucks with optimized scheduling requires 300 kilowatts instead of 1.5 megawatts if charging is distributed across nighttime hours rather than concentrated immediately upon return to depot.⁸ This load management directly translates to infrastructure cost avoidance and rate impact mitigation.

Class 8 heavy-duty electric trucks consume approximately 100,000-120,000 kilowatt-hours per year—equivalent to nine to eleven average U.S. homes annually.⁹ Light-duty EVs by comparison consume 3,000-4,000 kilowatt-hours per year. California projects 157,000 medium and heavy-duty vehicles by 2030, requiring 114,500 additional chargers beyond the million-plus needed for passenger vehicles.

More than 100 electric medium and heavy-duty truck models are now available, with federal heavy-duty emissions regulations anticipating zero-emission vehicle sales shares reaching up to 60% by 2032 in different segments.¹⁰ Purchase price parity with diesel is expected by 2028 for some segments, removing the primary adoption barrier.¹⁰

The market inflection point centers on 2028-2032, when heavy-duty economics align with passenger vehicle scale and commercial fleet commitments converge. Grid planners face a compressed window—2025-2028—to establish managed charging infrastructure before this wave materializes. Heavy-duty depot interconnections currently take up to two years, meaning fleet operators planning 2028-2030 electrification require infrastructure construction beginning now.

International Lessons: Norway’s Solution and China’s Warning

China’s experience with EV adoption at unprecedented scale offers both inspiration and warning. The world’s largest EV market has deployed more than 20 million electric vehicles, achieving 47.2% market share in 2024.¹ Unregulated ultra-fast charging could raise China’s peak loads by 70-85% by 2030, with peak loads potentially multiplying by 7.5 times by 2050.¹ The National Development and Reform Commission issued a dynamic pricing blueprint in January 2024, attempting to shift charging behavior after infrastructure deployment rather than integrating load management from the outset. The lesson for U.S. planners: managed charging infrastructure must precede mass adoption, not follow it.

Norway provides the counterpoint—demonstrating that even extreme EV penetration levels can integrate successfully with proper planning. At 94% EV market share, Norway leads the world in per-capita electrification yet faces manageable grid impacts through smart charging architecture.⁶ Analysis of a Norwegian city of 50,000 people with full EV adoption found that deployment without smart charging would require £200 million in grid investment, while managed charging enabled the same EV penetration with zero additional infrastructure investment.⁶

Norway’s solution architecture combines battery storage at charging locations for trickle charging from the grid with rapid discharge during vehicle charging events, avoiding grid destabilization. Local dynamic load management accounts for other consumption patterns on the same circuit, potentially increasing EV charging capacity on a site by up to eight times without infrastructure upgrades.⁶

California’s scale comparison illuminates U.S. infrastructure challenges. The state’s 2.1 million cumulative EVs exceed Norway’s approximately 647,000 and the Netherlands’ roughly 700,000 vehicles combined—despite lower market penetration rates. California and Norway share similar land areas, yet California’s population is seven times larger. This creates different grid stress patterns: Norway faces concentrated infrastructure challenges in smaller service areas, while California’s distributed geography demands infrastructure spanning vast distances with high per-capita EV density in urban cores.

The strategic insight from international experience is consistent: managed charging infrastructure isn’t optional at scale. Norway proves it reduces infrastructure costs to near-zero even at 94% penetration. China demonstrates the consequences of reactive rather than proactive grid integration.

The Path Forward: Strategic Integration Before 2028

The United States faces a compressed window to establish EV grid integration architecture before heavy-duty electrification and commercial fleet commitments converge. The strategic opportunity lies in establishing managed charging infrastructure, interconnection process reforms, and rate structures that capture the utilization paradox—transforming infrastructure investment into rate reduction.

California’s experience demonstrates that infrastructure costs, though substantial, are manageable when properly integrated. The state’s $26 billion distribution upgrade through 2035 supports 15.2 million EVs, yet net rate impact remains negative at $0.01-$0.06 per kilowatt-hour due to improved asset utilization.³ The challenge is deployment timing and managed charging penetration, not absolute cost.

Technology providers demonstrate that managed charging solutions exist and scale. WeaveGrid partners with nine of the ten largest U.S. utilities, Virtual Peaker offers holistic DER platforms, and multiple providers enable virtual power plant aggregation that unlocks up to $1,725 per vehicle annually in grid services value.⁵ The challenge shifts from technology availability to deployment penetration and regulatory enablement.

Electric vehicles represent the grid’s second infrastructure challenge after data centers, but the nature of EV load—flexible, distributed, and potentially bidirectional—creates opportunities data centers cannot match. The question isn’t whether the grid can accommodate EV adoption at scale. Norway, China, and California prove it can. The question is whether the United States will architect integration that transforms distributed batteries from burden into asset, capturing grid services value while driving rates down through improved utilization.

The infrastructure investment is coming regardless. The strategic choice is whether that investment delivers rate reduction and grid services or merely accommodates load growth. China chose reactive accommodation. Norway chose proactive integration. The American approach remains undetermined, with the 2025-2028 period likely decisive.

References

Nature Communications. “Impact of urban electric vehicle ultra-fast charging on grid stability.” 2024. https://www.nature.com/articles/s41467-024-urban-ev-charging

Chen, Yiyuan, Goutham Kukkadapu, et al. “Impact of electric vehicle charging demand on power distribution grid congestion.” Proceedings of the National Academy of Sciences. May 7, 2024. https://www.pnas.org/doi/10.1073/pnas.2317599121

Natural Resources Defense Council / Synapse Energy Economics. “Electric Vehicles Are Driving Rates Down.” NRDC. 2023-2024. https://www.nrdc.org/bio/max-baumhefner/electric-vehicles-are-driving-rates-down

Rystad Energy. “Data Centers and EV expansion create around 300 TWh increase in US electricity demand by 2030.” Rystad Energy. 2024. https://www.rystadenergy.com/news/data-and-ev-create-300-twh-increase-us

Industry analysis. “Orchestrating flexible BTM assets can unlock up to $1,725 per EV per year.” Multiple sources including VPP providers and utility studies. 2024.

Analysis cited in multiple sources. “Norwegian city of 50,000 with full EV adoption: £200M grid investment without smart charging vs. zero with managed charging.” Current, McKinsey, DNV. 2024. https://www.current.eco/norway-ev-smart-charging

IEEE Spectrum / Georgia Tech Center for Distributed Energy. “Transformer lifespan reduction from uncoordinated EV charging.” IEEE Spectrum. 2024. https://spectrum.ieee.org/the-ev-transition-explained-2658463709

NREL / TeraWatt Infrastructure / Fleet Owner. “Heavy-duty EV charging power requirements and home equivalents.” Multiple sources. 2024. https://www.nrel.gov/heavy-duty-ev-charging

Author calculation based on NREL estimates and EIA data. Class 8 truck annual consumption 100,000-120,000 kWh divided by average home 10,791 kWh.

International Energy Agency. “Global EV Outlook 2025.” IEA. May 14, 2025. https://www.iea.org/reports/global-ev-outlook-2025