How AI Data Centers Are Driving a $42 Billion Onsite Generation Boom

Supply chain crisis in gas turbines creating unprecedented opportunities for distributed generation

The data center industry is experiencing its most dramatic transformation since the dawn of cloud computing. By 2030, 27% of data center facilities are expected to be fully powered by onsite generation—a staggering increase that has resulted from the failure of grid investments in the US to keep up with this wave of demand, leading to 3-7 year waits to interconnect large data centers [1]. This isn't just another technology trend; it's a fundamental restructuring of how the world's most critical digital infrastructure gets its power.

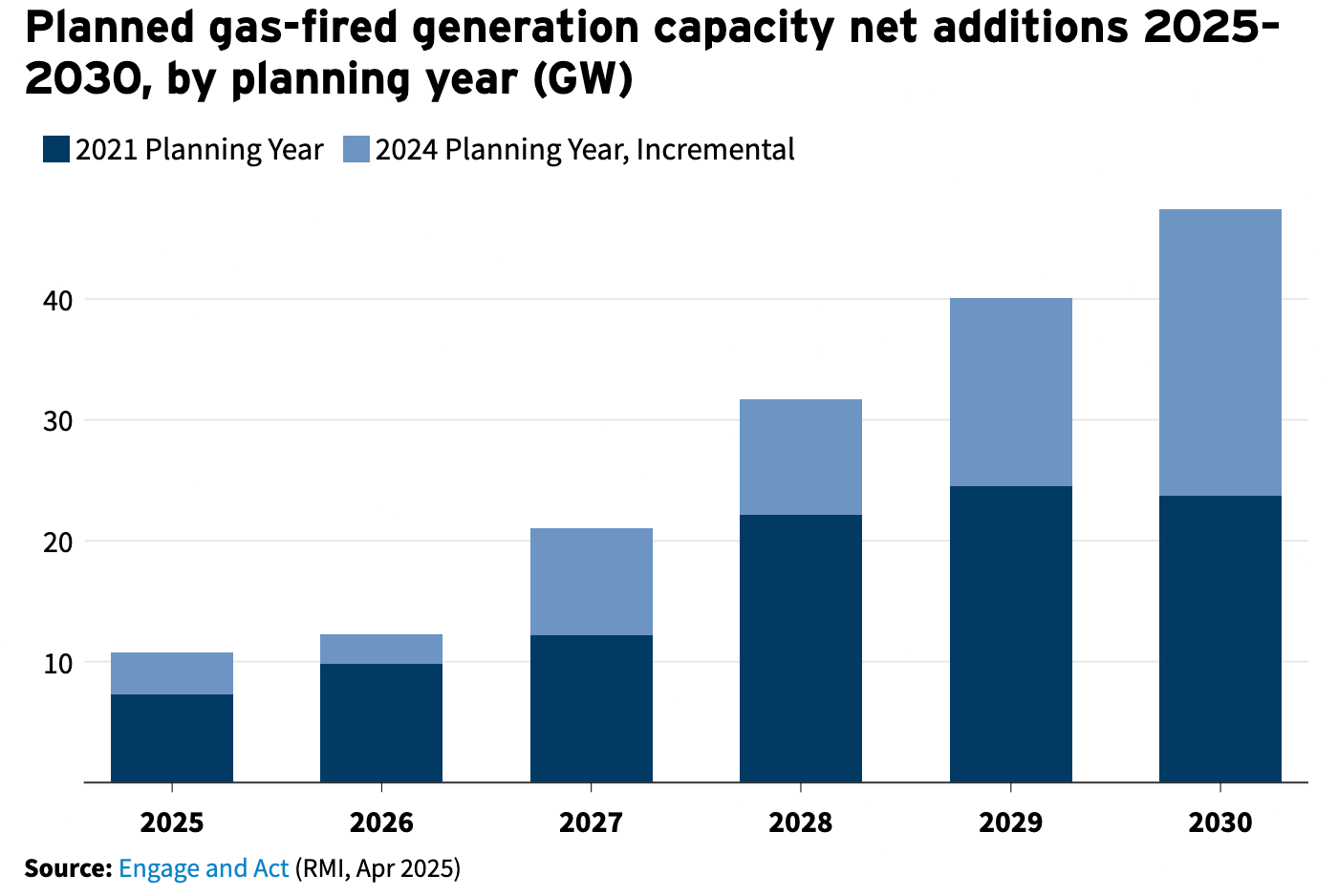

The catalyst? A supply chain crisis that has pushed gas turbine delivery times beyond 2029, creating an unprecedented window for distributed generation technologies. When Mitsubishi Power tells customers that turbines ordered today won't arrive until 2030, and GE Vernova pushes deliveries past 2029, the math becomes simple: AI data centers can't wait eight years for power[2]. The result is a $42 billion market by 2030, up from $20.21 billion today, driven by technologies that can deploy in months rather than years[3].

The implications stretch far beyond faster deployment. We're witnessing the emergence of what industry insiders call "power-first development"—where site selection begins with available generation capacity rather than proximity to fiber or customers. When 84% of data center operators rank power availability among their top three site selection factors, the companies that control their own power control their destiny[1].

When giants stumble, entrepreneurs sprint

The stranglehold of the "Big Three" gas turbine manufacturers—GE Vernova, Siemens Energy, and Mitsubishi Power—has created the most significant supply chain opportunity in modern industrial history. These companies control over 75% of the global gas turbine market, with Mitsubishi Power alone commanding 36% market share[5]. Their backlog? A staggering $148 billion at Siemens Energy alone[6].

But here's where the story gets interesting. These manufacturers just starting to announce investments to expand capacity amidst the booming demand, the slow response likely due to the dynamics of supply and demand favoring the incumbents as prices skyrocket. The Big Three are effectively rationing supply, creating premium pricing for queue jumping while skeptical about sustained demand from what they view as speculative data center projects. The cost escalation has been breathtaking. In 2022, combined cycle gas-fired construction costs averaged $722 per kilowatt, according to the US Energy Information Administration. Today, industry data shows costs of $2,200 to $2,500 per kilowatt for combined cycle configurations [7]. This represents a 200-300% increase in just three years—a cost spiral that's making onsite generation alternatives increasingly attractive by comparison.

This strategic miscalculation has opened the door for distributed generation technologies that can scale rapidly. While gas turbine manufacturers worry about overbuilding capacity, companies like Mainspring Energy are expanding manufacturing with a new plant in Pennsylvania [8], and reciprocating engine manufacturers are investing hundreds of millions in new capacity. The contrast couldn't be starker: established players defending margins while insurgents capture market share.

The speed differential is breathtaking. Bloom Energy can deploy fuel cell systems in 90 days. Reciprocating engines take 12-24 months. Gas turbines? That would be 2028-2030 for delivery, assuming you can even get in the queue[9]. Try explaining that timeline to a hyperscaler racing to deploy the next generation of AI infrastructure.

The rise of the new generation workhorses

Reciprocating engines are having their moment. After decades playing second fiddle to turbines in utility-scale power, they're perfectly positioned for the data center revolution. Caterpillar's Q2 power generation sales grew 19% driven by strong data center demand. The company recently announced a $725m investment in their Lafayette Engine Center, the largest since 1982[10].

The technology advantages are compelling. Caterpillar's G3520K fuel flexible engines deliver 2.5 MW per unit with high electric and thermal efficiency and the ability to ramp to full power in less than 5 minutes, a critical advantage for variable AI workloads[11]. These engines are planned for the massive 4GW data center in Utah developed by Joule Capital and with a first phase planned to be operational next year, which will incorporate Combined Cooling Heat and Power (CCHP) for maximum efficiency [11].

Clarke Energy is pioneering hybrid configurations that combine the instant response of battery storage with the duration of gas engines. Their hybrid power solutions demonstrate how battery systems can provide millisecond response for power quality while engines deliver sustained power for hours—a configuration perfectly suited to AI workloads that create sudden demand spikes followed by extended computational periods[12]. It's a configuration perfectly suited to AI workloads that create sudden demand spikes followed by extended computational periods. For more on batteries for data centers, see our previous Substack report.

Jenbacher is pushing fast-start capabilities to new extremes. Their J620 engines can deliver 3.3MW in under 45 seconds—faster than most gas turbines can even begin their startup sequence[13]. For data centers where every second of downtime costs thousands in lost revenue, that startup time becomes a competitive moat.

But perhaps most importantly, reciprocating engines offer fuel flexibility that turbines struggle to match. 2G Energy's North American expansion centers on engines that can switch between natural gas, hydrogen, and biogas without hardware changes[14]. When hydrogen infrastructure arrives—and it will—these engines will be ready.

The fuel cell insurgency reaches commercial scale

While engines grab headlines with their familiar roar, fuel cells are quietly revolutionizing data center power with the stealth of a technological ninja. Bloom Energy's deployments read like a who's who of hyperscale computing: over 100MW across 19 Equinix data centers, expanding Oracle partnerships, and a 1GW supply agreement with American Electric Power[15].

The performance metrics are impressive. Bloom Energy targets 3-9s to 5-9s reliability (99.9% to 99.999% uptime) while delivering 100MW per acre power density—double that of competing technologies[16]. Microsoft had an early commitment to decarbonization and was a leader in exploring fuel cells. Microsoft successfully powered server racks for 48 consecutive hours using 250kW hydrogen fuel cells back in 2020, moving the technology towards acceptance for primary power systems. Microsoft then scaled up to a 3MW fuel cell installation to demonstrate viability to replace diesel gensets [17].

Mainspring Energy represents the next evolution with linear generator technology that eliminates the rotating machinery plaguing traditional engines. Their systems deliver near-zero NOx emissions—a game-changer for permitting in non-attainment areas where 46% of planned data center sites are located[18]. When regulatory approval can take longer than construction, eliminating permitting bottlenecks becomes a strategic advantage worth millions.

The fuel flexibility story gets even better. Mainspring's linear generators can switch between natural gas, hydrogen, ammonia, and biogas without hardware changes. The 2G engines are fuel flexible and most fuel cells could run directly on hydrogen if it is available. As renewable energy creates more curtailed electrons that need conversion to storable hydrogen, these systems become the bridge between today's gas infrastructure and tomorrow's hydrogen economy. It’s a long shot, but maybe hydrogen will happen in a green and affordable way.

Geography determines destiny in the new power landscape

The regulatory arbitrage opportunities are staggering for developers who understand the geographic nuances. Texas offers a 100% exemption from the 6.25% state sales tax for qualifying data centers, while ERCOT's isolated grid enables faster interconnection—assuming you can handle the reliability challenges exposed during the 2021 winter storm[20].

If high electricity prices weren’t enough, California presents the regulatory complexity that's driving developers to seek alternatives. A number of bills have been introduced to put restrictions on data centers (many in an attempt to protect the rest of electricity rate payers) [21]. When 46% of planned data center sites fall in non-attainment zones requiring stricter emissions controls, fuel cells' near-zero emissions profile becomes worth millions in avoided compliance costs.

Virginia's dominance—35% of global hyperscale data centers processing 70% of world's internet traffic—is under pressure from local pushback[22]. Loudoun County residents face projected utility bill increases of $14-37 monthly by 2040 to support data center growth, creating political pressure for solutions that reduce grid dependence[23]. Onsite generation doesn't just solve power problems; it solves political problems.

The European comparison reveals where US markets are heading. Germany's Energy Efficiency Act requires existing data centers to achieve Power Usage Effectiveness (PUE) 1.5 by 2027 and 1.3 by 2030, while new centers must hit PUE 1.2 from 2026[24]. These aren't voluntary targets—they're binding legal requirements that make high-efficiency onsite energy essential for compliance.

When time is money, deployment speed becomes everything

The economic case for onsite generation transcends simple cost-per-kilowatthour calculations. It's about speed to market in an industry where first-mover advantage determines market share. Meta's Socrates project in Ohio demonstrates the scale of commitment: a $1.6 billion investment in 200MW of dedicated onsite generation, supplied by dedicated gas pipelines and isolated from grid vulnerabilities[25].

xAI's Memphis facility showcases the new deployment paradigm. Elon Musk's team built a 200,000 H100 GPU supercomputer in 122 days using 35+ mobile gas turbines and Tesla Megapack systems[26]. When expansion plans call for 1 million GPUs requiring 1.2GW—more power than some small cities—the ability to deploy generation at startup speed becomes the ultimate competitive advantage.

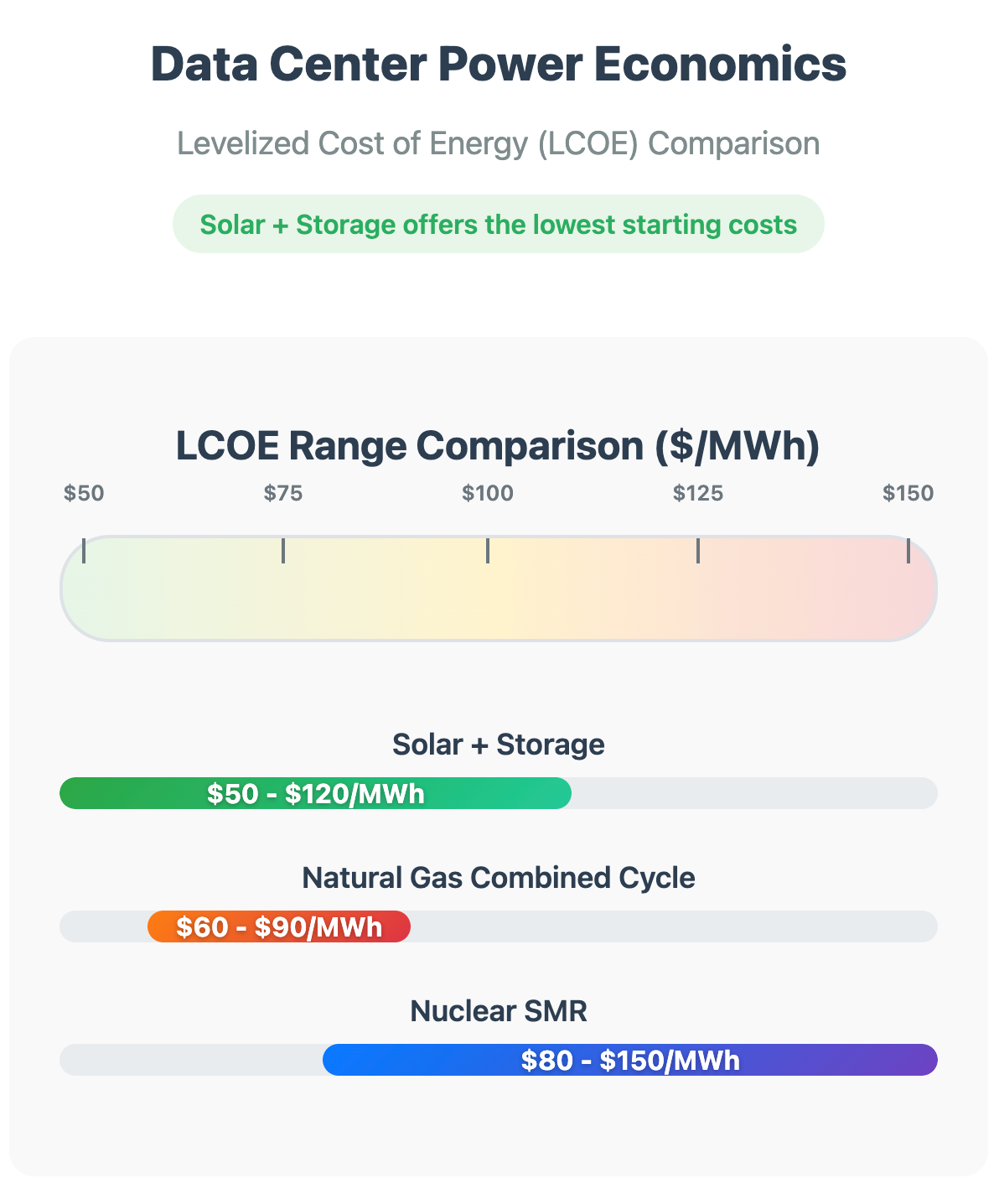

The LCOE calculations favor onsite generation when time value is properly accounted. Fuel cells operational in 90 days versus gas turbines delivered in 2030 means six additional years of revenue generation. At current AI compute pricing, that time advantage is worth hundreds of millions per project. The capital cost premium disappears when measured against operational cash flow.

Load-following capabilities add another dimension to the economic equation. AI workloads create power demand fluctuations that grid operators struggle to manage. Mainspring's linear generators provide millisecond response times that match computational demand in real time[27].

The hydrogen future arrives ahead of schedule

The technology roadmaps are converging on hydrogen faster than most industry observers anticipated. 2G Energy deployed North America's first 100% hydrogen CHP system in partnership with Enbridge Gas, demonstrating commercial viability today rather than theoretical future potential[28]. Jenbacher engines already operate on 60% hydrogen blends with plans for 100% hydrogen capability up to 1MW[29].

The infrastructure development timeline is accelerating. Hydrogen fuel cell costs have dropped since 2018, while electrolyzer costs continue falling as manufacturing scales[31]. When renewable energy curtailment reaches significant levels—and it will as solar and wind penetration grows—converting excess electrons to hydrogen becomes economically attractive.

Environmental compliance strategies increasingly favor hydrogen-ready systems. NOx regulations in non-attainment areas create 25-50 ton annual limits that trigger major source review processes[32]. Fuel cells' zero combustion emissions eliminate regulatory risk entirely, while hydrogen-capable engines future-proof against tightening standards.

The investment thesis crystallizes around speed and control

The venture capital flows tell the story with remarkable clarity. Mainspring Energy closed $258 million in Series F funding in April 2025, while the broader AI infrastructure investment market reached $45 billion in 2024—nearly doubling from $24 billion in 2023[33]. Late-stage deal sizes for GenAI companies continued to grow in 2024, reflecting the massive capital requirements for AI infrastructure[34].

Private equity is mobilizing unprecedented capital. Blackstone's $70 billion data center portfolio includes an additional $100 billion pipeline, while KKR and ECP formed a $50 billion partnership specifically for data center infrastructure[35]. When that much institutional capital targets a sector, the technology providers positioned for rapid deployment capture disproportionate value.

The strategic equation is straightforward: companies that control their power supply control their deployment timeline. In a market where hyperscalers announce 134GW of proposed data centers—up from 50GW a year ago—the ability to deploy independent of grid constraints becomes worth billions[36].

The technology leaders are positioning aggressively. Investments are being made across the board–fuel cells, linear generators, reciprocating engines, turbines–as the rush is on to capture market share in this massive wave of investment to build data center infrastructure for AI.

Conclusion: Tomorrow's power infrastructure is being built today

The data center industry stands at an inflection point that will define the next decade of digital infrastructure. The combination of AI-driven demand growth, supply chain constraints in traditional generation, and breakthrough improvements in distributed technologies has created a perfect storm of opportunity.

The numbers are staggering: global data center power capacity will triple from 81GW in 2024 to 277GW by 2035, representing 4.5% of global electricity demand rising to 8.7% by 2050[38]. This isn't incremental growth—it's the creation of an entirely new sector of the global economy.

The technology trajectories are converging. Fuel cells provide the fastest deployment and highest power density. Reciprocating engines offer proven reliability with rapid fuel switching capability. Hybrid systems combine the best characteristics of multiple technologies. All three approaches enable the speed-to-market that AI infrastructure demands. Behind the meter power is having a whole new era, thanks to the unstoppable demand of AI data center compute.

The regulatory environment increasingly favors distributed generation. State-level policies reward energy independence, federal regulations support grid modernization, and environmental compliance drives adoption of cleaner technologies. The companies that navigate this landscape successfully will build lasting competitive advantages.

But perhaps most importantly, the market is finally large enough to support multiple technology winners. A $42 billion market growing at 13.2% annually can accommodate breakthrough companies across multiple technology platforms[39]. The question isn't whether onsite generation will transform data center power—it's which technologies will capture the most value in the transformation.

The reciprocating engine revolution is just the beginning. The real story is how an entire industry is reimagining its relationship with power, choosing speed over scale, control over cost, and independence over integration. And within this story, distributed generation technologies are enabling a fundamental restructuring of the relationship between data centers and the grid. In a world where data is the new oil, the companies that control their own refineries will write the future.

The transformation is already underway. The only question is which companies will capture the most value as the $6.7 trillion global infrastructure opportunity unfolds over the next decade.

Footnotes

Bloom Energy, "Onsite Generation Expected to Fully Power 27% of Data Center Facilities by 2030." https://www.bloomenergy.com/news/onsite-generation-expected-to-fully-power-27-percent-of-data-center-facilities-by-2030/

Rocky Mountain Institute, "Gas Turbine Supply Constraints Threaten Grid Reliability; More Affordable Near-Term Solutions Can Help." https://rmi.org/gas-turbine-supply-constraints-threaten-grid-reliability-more-affordable-near-term-solutions-can-help/

Grand View Research, "Data Center Power Market Size, Share | Industry Report, 2030." https://www.grandviewresearch.com/industry-analysis/data-center-power-market

Data Center Frontier, "Onsite Power for Data Centers: How to Choose the Right Solution." https://www.datacenterfrontier.com/sponsored/article/55276009/onsite-power-for-data-centers-how-to-choose-the-right-solution

Global Energy Monitor, "Leading Three Manufacturers Providing Two-thirds of Turbines for Gas-fired Power Plants Under Construction." https://globalenergymonitor.org/report/leading-three-manufacturers-providing-two-thirds-of-turbines-for-gas-fired-power-plants-under-construction/

Siemens Energy, "Earnings Release Q3 FY 2025." https://www.siemens-energy.com/global/en/home/investor-relations.html

S&P Global, “US gas-fired turbine wait times as much as seven years; costs up sharply”, May 20, 2025, https://www.spglobal.com/commodity-insights/en/news-research/latest-news/electric-power/052025-us-gas-fired-turbine-wait-times-as-much-as-seven-years-costs-up-sharply

Mainspring Energy, https://www.mainspringenergy.com/news/us-doe-awards-mainspring-$87-million-manufacturing-grant/

Data Center Frontier, "Onsite Power for Data Centers: How to Choose the Right Solution." https://www.datacenterfrontier.com/sponsored/article/55276009/onsite-power-for-data-centers-how-to-choose-the-right-solution

Caterpillar, "Caterpillar Expands Lafayette Large Engine Center," August 13, 2024. https://www.caterpillar.com/en/news/corporate-press-releases/h/lafayette-large-engine-expansion.html

Energy Storage News, "Caterpillar signs deal for CHP plant with 1.1GWh integrated BESS at data centre campus in Utah,” August 8, 2025, https://www.energy-storage.news/caterpillar-signs-deal-for-chp-plant-with-1-1gwh-integrated-bess-at-data-centre-campus-in-utah/

Clarke Energy, "Battery Energy Storage Solutions (BESS)." https://www.clarke-energy.com/us/battery-energy-storage-systems-bess/

Jenbacher, "Data Center Power Solutions." https://www.jenbacher.us/en/our-solutions/industries/data-centers

2G Energy, "Combined Heat and Power Solutions." https://www.2g-energy.com/

Bloom Energy, "Bloom Energy Expands Data Center Power Agreement with Equinix Surpassing 100MW." https://www.bloomenergy.com/news/bloom-energy-expands-data-center-power-agreement-with-equinix-surpassing-100mw/

Bloom Energy, "Reliable Data Center Power Solutions." https://www.bloomenergy.com/industries/data-center-power/

Data Center Dynamics, "Microsoft builds 3MW hydrogen fuel cell backup power plant,” July 29, 2022, https://www.datacenterdynamics.com/en/news/microsoft-builds-3mw-hydrogen-fuel-cell-backup-power-plant/

Data Center Frontier, "Onsite Power for Data Centers: How to Choose the Right Solution." https://www.datacenterfrontier.com/sponsored/article/55276009/onsite-power-for-data-centers-how-to-choose-the-right-solution

Mainspring Energy, "Data Centers." https://www.mainspringenergy.com/solutions/data-center/

Texas Comptroller, "Data Centers Tax Exemptions." https://comptroller.texas.gov/taxes/data-centers/

Manatt, "California Legislation Introduced Impacting Data Centers Amid Concerns Over Resource Use." https://www.manatt.com/insights/newsletters/california-legislation-introduced-impacting-data-centers-amid-concerns-over-resource-use

Virginia Economic Development Partnership, "Data Centers." https://www.vedp.org/industry/data-centers

Virginia Joint Legislative Audit and Review Commission, "Data Centers in Virginia." https://jlarc.virginia.gov/landing-2024-data-centers-in-virginia.asp

European Commission, "Commission adopts EU-wide scheme for rating sustainability of data centres." https://energy.ec.europa.eu/news/commission-adopts-eu-wide-scheme-rating-sustainability-data-centres-2024-03-15_en

Power Magazine, "New 200-MW Gas-fired Plant in Ohio Will Power Meta Data Center." https://www.powermag.com/new-200-mw-gas-fired-plant-in-ohio-will-power-meta-data-center/

CNBC, "Musk's xAI scores permit for gas-burning turbines to power Grok supercomputer in Memphis." https://www.cnbc.com/2025/07/03/musks-xai-gets-permit-for-turbines-to-power-supercomputer-in-memphis.html

Mainspring Energy, "Data Centers." https://www.mainspringenergy.com/solutions/data-center/

2G Energy, "2G and Enbridge Gas Collaborate for North America's First 100% H2 CHP." https://blog.2g-energy.com/2g-and-enbridge-gas-collaborate-for-north-americas-first-100-h2-chp

Jenbacher, "Energy Solutions for Data Centers." https://www.jenbacher.com/en/energy-solutions/industries/data-center

Data Center Knowledge, "Microsoft Claims First Hydrogen-Fueled Data Center Test." https://www.datacenterknowledge.com/microsoft/microsoft-claims-first-hydrogen-fueled-data-center-testMicrosoft Claims a First in Hydrogen-Fueled Data Center Test

Microsoft, "Microsoft tests hydrogen fuel cells for backup power at datacenters." https://news.microsoft.com/innovation-stories/hydrogen-datacenters/

Cummins, "Data centers are reducing their NOx emissions." https://www.cummins.com/news/2023/08/11/data-centers-are-reducing-their-nox-emissions

PR Newswire, "Mainspring Secures $258 Million in Financing to Scale Linear Generator Business." https://www.prnewswire.com/news-releases/mainspring-secures-258-million-in-financing-to-scale-linear-generator-business-adds-energy-and-tech-leaders-to-board-302426971.html

Crunchbase News, "AI, Data Center And Energy Startups Raised $4B In October 2024." https://news.crunchbase.com/venture/ai-data-center-energy-startups-funding-october-2024/

Data Center Dynamics, "Blackstone's prospective data center pipeline hits $100bn, on top of $70bn portfolio" https://www.datacenterdynamics.com/en/news/blackstones-prospective-data-center-pipeline-hits-100bn-on-top-of-70bn-portfolio/

Wood Mackenzie, "US power struggle: how data centre demand is challenging the electricity market model." https://www.woodmac.com/horizons/us-data-centre-power-demand-challenges-electricity-market-model/

Bloom Energy, "Reliable Data Center Power Solutions." https://www.bloomenergy.com/industries/data-center-power/

BloombergNEF, "Power for AI: Easier Said Than Built." https://about.bnef.com/insights/commodities/power-for-ai-easier-said-than-built/

Grand View Research, "Data Center Power Market Size, Share | Industry Report, 2030."https://www.grandviewresearch.com/industry-analysis/data-center-power-market