Data Centers: From Grid Burden to Strategic Asset

How AI demand is transforming computing infrastructure into billions in grid flexibility

Data centers are no longer passive power consumers—they’re becoming active grid participants capable of delivering 5-15 GW of dispatchable capacity through strategic curtailment. This represents the equivalent of 15-45 large power plants while simultaneously meeting unprecedented AI-driven electricity demand. The transformation fundamentally reshapes how critical infrastructure supports grid reliability, unlocked by a convergence of surging power demand, advanced control technologies, and multi-billion dollar market incentives.

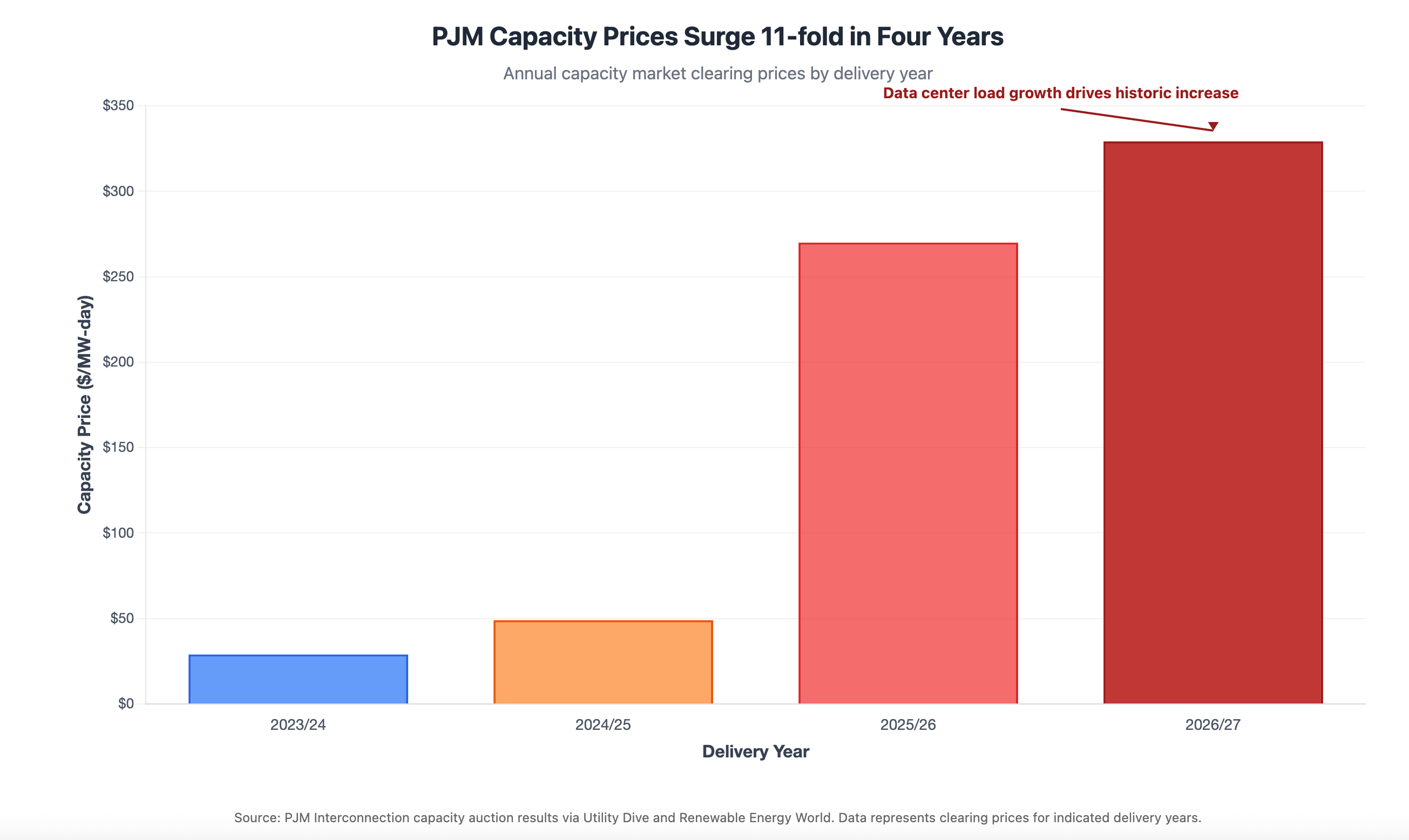

Consider the economic pressure driving this shift: PJM Interconnection’s capacity market prices surged from $28.92/MW-day to $329.17/MW-day for 2026/27 delivery¹—an 11-fold increase that translates to billions in annual costs. Meanwhile, U.S. data center capacity will add 65 GW through 2029², creating both crisis and opportunity.

The companies mastering grid-interactive operations will capture significant competitive advantages through faster interconnection, reduced capacity costs, and new revenue streams from flexibility services.

The strategic opportunity: technical capability meets market incentive

The technical foundation for grid-interactive data centers has matured dramatically. Unlike traditional industrial loads, data centers possess inherent flexibility through sophisticated power infrastructure, redundant systems, and workload management capabilities. While Tier IV facilities target 99.995% uptime, most cloud and AI workloads achieve reliability through geographic redundancy rather than individual site availability. This architectural approach unlocks flexibility impossible for traditional colocation or enterprise facilities.

Three distinct mechanisms enable grid participation without compromising operations. Grid-interactive UPS systems provide bidirectional power flow for frequency regulation, charging and discharging based on grid signals while maintaining full backup capability with sub-second response times. Workload flexibility delivers the largest potential through computational load management—shifting computation timing between facilities, moving workloads geographically, or reducing computation intensity during peak periods. On-site backup generators add dispatchable capacity during emergencies, with recent regulatory clarifications enabling limited grid support though EPA restrictions still constrain broader participation.

The economics are compelling. Duke University’s Nicholas Institute analysis demonstrates that existing U.S. generation capacity can integrate nearly 100 GW of new flexible loads with minimal grid impact³, assuming 5-10% curtailment capability for 50-100 hours annually—roughly 1% of operational time. This “curtailment-enabled headroom” can accommodate substantial data center growth without premature infrastructure investment. Realizing this potential requires coordinated flexibility and optimal geographic distribution, but the value proposition is clear: data centers trade brief operational constraints for deployment speed, connecting in 12-18 months versus 5-8 years for traditional generation or pursuing onsite generation alternatives.

Market compensation structures make flexibility increasingly attractive. PJM’s capacity market alone generates $120,000+ in annual revenue per MW of certified capacity at current clearing prices. ERCOT’s new Contingency Reserve Service, CAISO’s expanding Western Energy Imbalance Market, and MISO’s reliability-based demand curve all create substantial revenue opportunities. Revenue stacking enables multiple value streams from the same flexibility assets—capacity markets, energy optimization, frequency regulation, and emergency curtailment programs maximize returns on grid-interactive capabilities.

Hyperscalers prove technical and economic viability

Google’s demand response program represents the most comprehensive implementation, demonstrating both technical feasibility and economic value at scale. During the 2022-23 European energy crisis, facilities in the Netherlands, Belgium, Ireland, Finland, and Denmark provided daily power reductions. U.S. implementations include successful partnerships with Omaha Public Power District, where Google reduced machine learning workload power during grid events in 2024, plus new agreements with Indiana Michigan Power and Tennessee Valley Authority specifically targeting AI workload flexibility⁴.

The key insight: Google achieves these reductions with zero service level agreement violations through geographic diversification and computational workload portfolios including deferrable tasks like indexing and model training. Advanced control systems integrate with multiple grid operators using machine learning algorithms that optimize power-performance relationships in real-time. The program proves large-scale operators with diverse workload portfolios can provide reliable grid services while maintaining operational requirements.

Microsoft’s Dublin data center pioneered different technical capabilities through grid-interactive UPS technology. Partnering with Enel X and EirGrid, the facility provides frequency regulation services while achieving 99.999% uptime—exceeding even Tier IV standards⁵. The implementation demonstrates how existing backup power infrastructure can deliver dual benefits: emergency resilience and grid stability services.

These implementations share critical characteristics enabling success. Both operators possess geographic diversification allowing workload migration during curtailment events. Both maintain sophisticated control systems integrating grid signals with operational management. Both operate workloads with temporal flexibility—training algorithms and batch processing rather than latency-sensitive inference. Smaller operators and those running primarily real-time applications face greater challenges replicating these results, though aggregation platforms may enable participation through portfolio effects.

The competitive landscape among flexibility resources matters strategically. Data centers compete with behind-the-meter battery storage offering similar response speed at higher capital cost, industrial demand response with decades of operational history, and emerging vehicle-to-grid programs with larger aggregate potential but greater coordination challenges. Data centers’ competitive advantage lies in response speed, geographic concentration simplifying grid integration, and co-location opportunities with generation reducing transmission constraints.

Strategic implications: infrastructure meets opportunity

The convergence of technical capability and market incentive creates strategic opportunities for data center operators, utilities, and grid operators. Flexible interconnection programs enable faster grid connection in exchange for curtailment capability—trading operational constraints for deployment speed addresses the substantial interconnection backlog exceeding total U.S. installed capacity.

Custom tariff designs exemplified by Indiana Michigan Power’s agreements with Google and Amazon create bespoke compensation structures aligned with AI workload characteristics. These arrangements recognize unique technical capabilities while delivering clear economic incentives, establishing templates for broader deployment.

Virtual power plant aggregation enables smaller data centers to participate in wholesale markets through specialized platforms. The aggregation model addresses minimum participation thresholds while creating portfolio effects improving reliability and predictability of demand response resources. As the virtual power plant market expands, data center aggregation represents a high-value opportunity for operators unable to pursue direct market participation.

Three critical barriers must be resolved for widespread deployment. Baseline measurement challenges complicate verification of load reductions without access to proprietary workload data—traditional demand response programs struggle with baseline gaming, and data centers’ highly variable computational loads make establishing credible baselines particularly difficult. Regulatory uncertainty around backup generator participation continues as EPA emissions restrictions limit annual operating hours while FERC Order 2222 implementation varies widely across regions. Workload type matters critically as AI deployments mature from flexible training workloads toward latency-sensitive inference, potentially narrowing the flexibility window.

Current market structures also undervalue many services data centers can provide. Grid formation services, distribution-level voltage support, and long-duration flexibility beyond typical 4-hour storage represent significant compensation gaps growing increasingly valuable as renewable penetration rises.

The path forward requires continued collaboration between data center operators, utilities, grid operators, and regulators developing standardized technical protocols, appropriate cost allocation mechanisms, and market structures fairly compensating the full value stack of grid-interactive capabilities. The companies and regions mastering this integration will capture competitive advantages in deployment speed, operational costs, and grid reliability.

The transformation of data centers from passive loads to strategic grid resources represents a fundamental paradigm shift. 5-15 GW of flexible capacity activated 50-100 hours annually can address 15-20% of projected demand growth in regions with mature demand response markets while deferring billions in transmission and generation investment. Hyperscaler implementations prove technical feasibility and economic viability. Evolving market mechanisms create sustainable business models. The strategic opportunity is clear—and the competitive race has begun.

References

Utility Dive. “PJM capacity prices set another record with 22% jump.” https://www.utilitydive.com/news/pjm-interconnection-capacity-auction-prices/753798/

Wilson, J. D., Z. Zimmerman, and R. Gramlich. “Strategic Industries Surging: Driving US Power Demand.” GridStrategies. 2024. https://gridstrategiesllc.com/wp-content/uploads/National-Load-Growth-Report-2024.pdf

Nicholas Institute for Energy, Environment & Sustainability, Duke University. “Rethinking Load Growth: How Flexible Loads Can Expand Grid Headroom and Accelerate Decarbonization.” February 2025. https://nicholasinstitute.duke.edu/publications/rethinking-load-growth

Google. “How we’re making data centers more flexible to benefit power grids.” https://blog.google/inside-google/infrastructure/how-were-making-data-centers-more-flexible-to-benefit-power-grids/

Microsoft. “Microsoft datacenter batteries to support growth of renewables on the power grid.” https://news.microsoft.com/source/features/sustainability/ireland-wind-farm-datacenter-ups/

Department of Energy. “DOE Releases New Report Evaluating Increase in Electricity Demand from Data Centers.” https://www.energy.gov/articles/doe-releases-new-report-evaluating-increase-electricity-demand-data-centers

Federal Energy Regulatory Commission. “FERC Order No. 2222 Explainer: Facilitating Participation in Electricity Markets by Distributed Energy Resources.” https://www.ferc.gov/ferc-order-no-2222-explainer-facilitating-participation-electricity-markets-distributed-energy